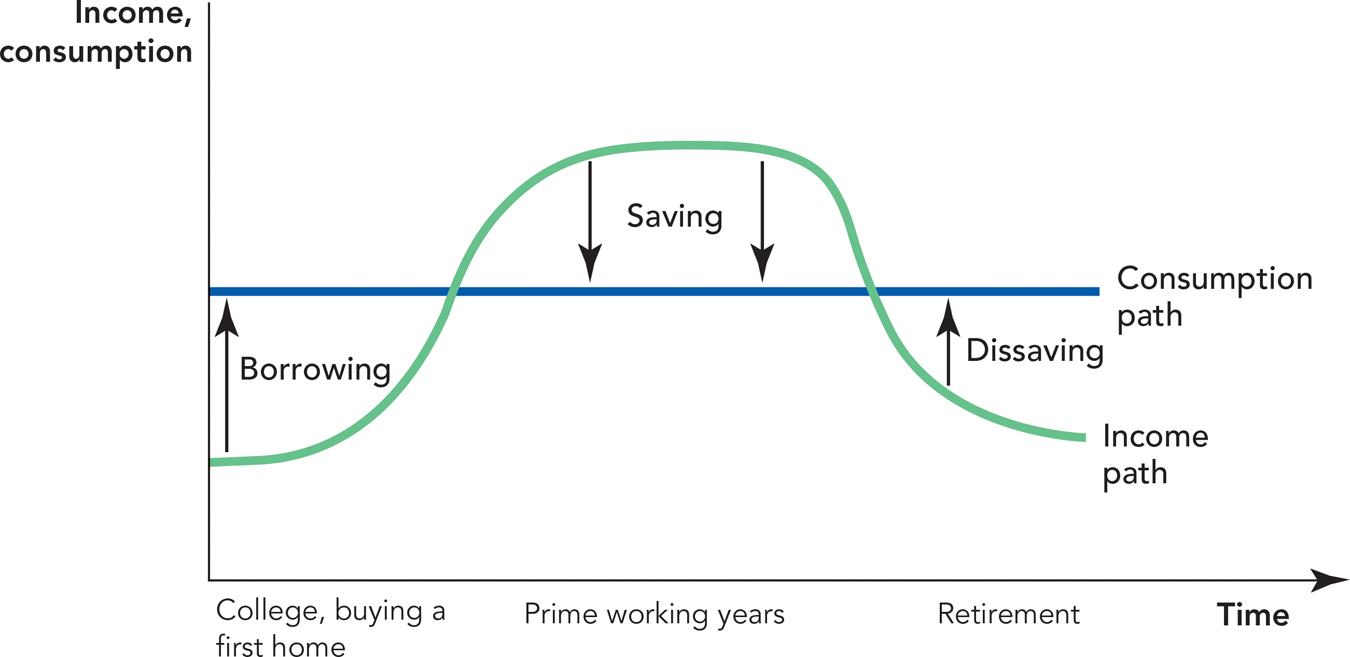

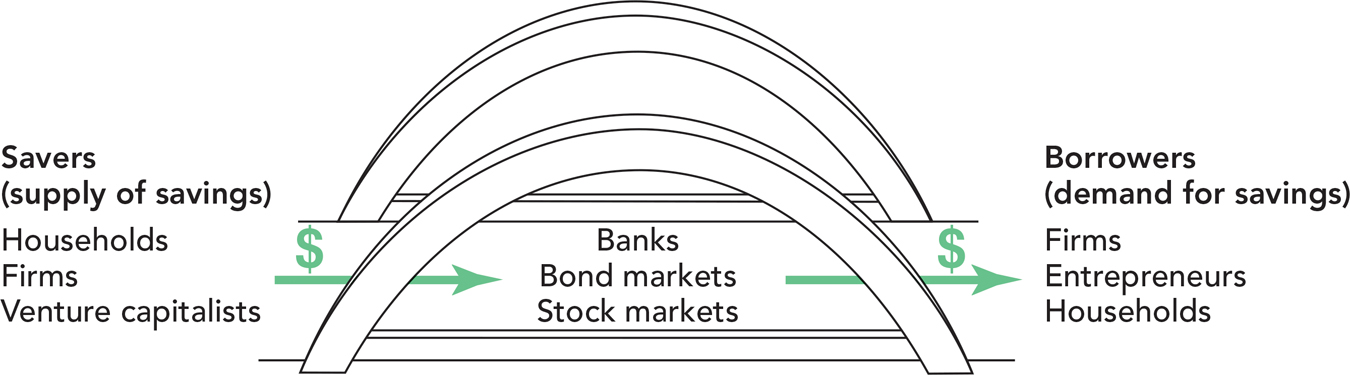

class: center, middle, inverse, title-slide # 4.5 — Factor Markets II: Capital ## ECON 306 · Microeconomic Analysis · Fall 2020 ### Ryan Safner<br> Assistant Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/microF20"><i class="fa fa-github fa-fw"></i>ryansafner/microF20</a><br> <a href="https://microF20.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>microF20.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Labor Market for Competitive Firm](#12) ### [Labor Market for a Monopoly](#30) ### [Monopsony Power](#34) ### [Monopoly Power in Labor Markets: Unions](#54) --- # What is Capital? .pull-left[ - A note on how we used capital `\(K\)` earlier this semester... - Assumed capital (essentially machines) has a market price `\(“r”\)`, the “rental rate of capital” - Most firms purchase machines outright, rather than rent them per period (e.g. per hour) - But like any input, we consider the (opportunity) cost of using a marginal unit of an input as its market price if it were exchanged on the market - Hence, consider the price of capital the market rate to rent a machine for an hour ] .pull-right[ .center[  ] ] --- # What is Capital? .pull-left[ - Exact nature & definition remains controversial to economists to this day - “Capital” is: - hard to define or (especially) aggregate - necessarily bound up with time and uncertainty ] .pull-right[ .center[  ] ] --- # What Is Capital? .pull-left[ .smallest[ - Economists (and others) often talk about different *types* of capital - .hi-turquoise[Physical capital]: tools, machines, specialized equipment, software, that makes labor more productive - .hi-turquoise[Human capital]: skills, training, education, experience embodied in a person that makes their labor more productive - .hi-turquoise[Financial capital]: access to immediate cash to finance investment for production - Social scientists also talk about “political capital,” “social capital,” etc... ] ] .pull-right[ .center[    ] ] --- # What Is Capital? .pull-left[ .smallest[ - Some generally observed features of capital: - .hi-turquoise[Capital is *not an original factor*] - It’s land & labor combined in the past (i.e. someone had to make the shovel, the factory, etc. with land & labor) - .hi-turquoise[Capital goods are not directly consumed] - Used in the production of other goods - .hi-turquoise[Capital inherently consists of a time element] - Makes labor more productive - Capital as “stored labor time” - Capital comes from **savings**, and earns **interest** ] ] .pull-right[ .center[  ] ] --- # What Is Capital? .pull-left[ .smallest[ - For our purposes today, let’s not think of capital as *physical* capital, but as financial capital - All types of capital have the following financial aspect - Capital is about .hi-purple[the diversion of present consumption towards future consumption] - Capital comes from savings, and is used for investments that firms (and households) use to increase their (production for) consumption - The return that owners of capital get for providing capital to firms is .hi[interest] ] ] .pull-right[ .center[  ] ] --- # What Is Capital? .pull-left[ - Historically, the idea came from farmers - During harvest time, can consume all produce today, or save some for next year - The more you save today, the less you can eat now, but the more you will have in the future - The more you consume today, the less you will have in the future ] .pull-right[ .center[  ] ] --- # Capital Markets .pull-left[ - Firms (and households) get money for investment today by participating in .hi[capital markets] - The funds in capital markets come from individual savings ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # The Time Value of Money --- # Present vs. Future Goods .pull-left[ - In discussing capital, we are comparing .hi-purple[present goods] with .hi-purple[future goods] - Futures: claims on goods to be delivered at a future date - corn futures, oil futures, etc. - Financial assets: bonds, lottery winnings, loans - Real goods: immature orchard of fruit trees; durable goods that yield output later ] .pull-right[ .center[  ] ] --- # Present vs. Future Goods .pull-left[ - .hi-purple[Interest rate is a price of future goods in terms of present goods] - How much individuals will pay to receive income now vs. later - .hi-purple[Investment in capital]: present consumption can be saved to buy/build machinery that can increase future income flows ] .pull-right[ .center[  ] ] --- # Present vs. Future Goods .pull-left[ - Consider goods-bundles consumed now vs. consumed at later date - i.e. not apples vs. oranges, but apples and oranges **today** vs. apples and oranges **next year** - .hi-purple[Agent's objective]: optimize time-profile of consumption, **maximize net present value** ] .pull-right[ .center[  ] ] --- # Present vs. Future Goods .pull-left[ .smallest[ - .hi-purple[Time Value of Money]: same nominal amount of money<sup>.magenta[†]</sup> is worth different amounts over time `$$\begin{align*} PV &= \frac{FV}{(1+r)^n}\\ FV &= PV(1+r)^n\\ \end{align*}$$` - `\(PV\)`: present value - `\(FV\)`: future value - `\(r\)`: interest rate - `\(n\)`: number of time periods ] .footnote[<sup>.magenta[†]</sup> Or income, or consumption...] ] .pull-right[ .center[  ] ] --- # Present vs. Future Goods .pull-left[ - .hi-green[Example]: what is the present value of getting $1,000 one year from now at 5% interest? `$$\begin{align*} PV &= \frac{FV}{(1+r)^n}\\ PV &= \frac{1000}{(1+0.05)^1}\\ PV &= \frac{1000}{1.05}\\ PV &= \$952.38\\ \end{align*}$$` ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-1-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Present vs. Future Goods .pull-left[ - .hi-green[Example]: what is the *future* value of $1,000 lent for one year at 5% interest? `$$\begin{align*} FV &= PV(1+r)^n\\ FV &= 1000(1+0.05)^1\\ FV &= 1000(1.05)\\ FV &= \$1050\\ \end{align*}$$` ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-2-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Rule of 72 .pull-left[ - A good rule of thumb: number of years for your principal to double: `$$\frac{72}{r}$$` - This is known as the .hi-purple[rule of 72]<sup>.magenta[1]</sup> .footnote[<sup>.magenta[1]</sup> Different people use other numbers, like 70. The point is more to make mental calculations easily rather than accurately.] ] .pull-right[ .center[  ] ] --- # Rule of 72 .hi-green[Example]: - If interest rate is 2%, your money doubles in `\(\frac{72}{2}=36\)` years -- - If interest rate is 3%, your money doubles in `\(\frac{72}{3}=24\)` years -- - If interest rate is 4%, your money doubles in `\(\frac{72}{4}=18\)` years -- - If interest rate is 6%, your money doubles in `\(\frac{72}{6}=12\)` years -- - Interest rate is very important price! Makes all the difference whether it is 1% vs. 2%! --- # Compounding Interest <img src="capital-slides_files/figure-html/unnamed-chunk-3-1.png" width="1008" style="display: block; margin: auto;" /> --- # Historical Interest Rates <img src="capital-slides_files/figure-html/unnamed-chunk-4-1.png" width="864" style="display: block; margin: auto;" /> --- class: inverse, center, middle # Individual Savings Decisions --- # Individual Savings Decisions .pull-left[ - The .red[Supply of Capital] comes from **individual decisions to save** - Sacing is considered a .hi[disutility] (a .hi[bad]) - **Opportunity cost** of saving is .hi[consumption] - But, saving (and lending) can earn .hi-purple[interest] - Tradeoff: if you save more, you consume less today, but can consume more in the future (with interest income) ] .pull-right[ .center[  ] ] --- # Individual Savings Decisions .pull-left[ - Apply our consumer choice model to .hi[“intertemporal” choice] to consume: `$$u(c_1,c_2)$$` - `\(c_1\)`: consumption today (period 1) - `\(c_2\)`: consumption tomorrow (period 2) - Define amount of saving as: `$$s = M - c_1$$` - where `\(M_0\)` is today’s income ] .pull-right[ .center[  ] ] --- # Individual Savings Decisions .pull-left[ .smallest[ `$$u(c_1,c_2)$$` - Individuals have a .hi[“time preference”] between present consumption and future consumption - In general, everyone prefers consumption today over consumption in the future - We place a .hi-purple[premium] on present consumption and .hi-purple[discount] future consumption - This is where the idea of .hi[interest] and the .hi-purple[time value of money] come from (more on those later) - A measure of how .hi[impatient] you are - High time preference: strong preference for present consumption, not willing to wait to future - Low time preference: more willing to defer present consumption to future ] ] .pull-right[ .center[  ] ] --- # Individual Savings Decisions .pull-left[ - Most people follow a consistent “life cycle” of saving decisions - People like to “smooth” their consumption over time, rather than experience sudden, discontinuous jumps in consumption level - When actual income `\(<\)` preferred consumption: .hi[borrow] money - When actual income `\(>\)` preferred consumption: .hi[save] (and .hi[lend]) money ] .pull-right[ .center[  ] ] --- # Individual Savings Decisions .pull-left[ `$$u(c_1,c_2)$$` - .hi-purple[Marginal rate of (intertemporal) substitution]: rate at which person gives up future consumption `\((c_1)\)` to obtain more present consumption `\((c_0)\)` - The slope of the indifference curve! ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-5-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions .pull-left[ .smnallest[ - Suppose individual starts with an income today `\(M_0\)` - Must choose how much of it to consume today `\((c_0)\)` versus save to consume more in future `\((c_1)\)` - Let individual have opportunities to exchange in .hi[capital markets] - Exchange present goods `\(c_0\)` for claims on future goods `\(c_1\)` repaid with interest at rate `\(r\)` - In extremes: can consume entirety of `\(M_0\)` today, or save entirety of `\(M_0\)` and earn interest to get `\(M_0(1+r)\)` consumption next year ] ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-6-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions .pull-left[ - .hi-purple[Opportunity cost] of consumption today `\((c_0)\)` is `\(1+r\)` - Forgo opportunity to save and invest to earn interest (and consume more) next period - Let the price of future consumption be $1 - Then the slope of .red[budget constraint] is `$$-\frac{p_{c_0}}{p_{c_1}}=-\frac{(1+r)}{1}=-(1+r)$$` ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-7-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions .pull-left[ - Consumer maximizes utility subject to budget constraint at `\(A\)`: `\((c_0^\star, c_1^\star)\)` ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-8-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions .pull-left[ - Consumer maximizes utility subject to budget constraint at `\(A\)`: `\((c_0^\star, c_1^\star)\)` - Consumes `\(c_0^\star\)` today, saving `\(\color{#6A5ACD}{s = M_0 - c_0^\star}\)` to consume `\(\color{#e64173}{c_1^\star = s(1+r)}\)` next period ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-9-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions: A Change in Interest Rate .pull-left[ .smaller[ - What will happen to the optimal savings decision if **interest rate `\(r\)` increases**? - It depends! - Consumption is a normal good, but this makes savings “inferior” `$$s = M_0 - c_0$$` - `\(\uparrow c_0 \implies \downarrow s\)` - Again, .hi-purple[income and substitution effects] are important! ] ] .pull-right[ .center[  ] ] --- # Individual Savings Decisions: A Change in Interest Rate .pull-left[ - .purple[(Overall) Price effect]: `\(A \rightarrow C\)` - Higher rate `\(r\)` leads to less consumption today `\(c_0\)` and therefore, more saving `\(s\)` - Upward sloping .red[savings supply curve] ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-10-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions: A Change in Interest Rate .pull-left[ - .orange[Substitution effect]: as interest rate `\(r\)` increases, the price of present consumption `\(c_0\)` is increasing, so consume less today - Thus, save more - Graphically: under higher rate `\(BC_2\)`, substitute more `\(c_1\)` for less `\(c_0\)` (more saving) holding utility constant - `\(A \rightarrow B\)`: more `\(c_1\)`, less `\(c_1\)` (more `\(s)\)` ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-11-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions: A Change in Interest Rate .pull-left[ - .green[Real income effect]: the higher interest rate makes you wealthier in real terms, so buy more of everything (including `\(c_0\)`, meaning **save less!**) - `\(B \rightarrow C\)`: attain higher indifference curve `\(\color{green}{u_2}\)` - “Inferior” good: higher interest rates induce *more* consumption today (and less saving) ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-12-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions: A Change in Interest Rate .pull-left[ - Income & substitution effects cut against each other - If .orange[Substitution effect] `\(>\)` .green[Income effect], then we get a positive .purple[price effect]: - **Increase in interest rate** causes .hi-purple[more saving] (less present consumption) - Matches our intuition, .red[upward-sloping savings supply curve] ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-13-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Individual Savings Decisions: A Change in Interest Rate .pull-left[ - If .green[Income effect] > .orange[Substitution effect], leading to a negative .purple[price effect]: - **Increase in interest rate** causes .hi-purple[less saving] (more present consumption) - “Giffen-style” scenario, but **plausible** for saving! (unlike consumer goods) - Intuition: imagine having an savings target (for rainy day, or retirement), and interest rates increase ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-14-1.png" width="504" style="display: block; margin: auto;" /> ] --- class: inverse, center, middle # The Market For Loanable Funds --- # The Market for Loanable Funds .pull-left[ - In general, an upward sloping .red[market supply curve] - Giving up money today in exchange for claim on future repayment with interest - Individuals that loan their savings are called .hi[capitalists] 🧐 - Individuals supply more (less) savings at higher (lower) interest rates ] .pull-right[ <img src="capital-slides_files/figure-html/unnamed-chunk-15-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Demand for Capital .pull-left[ - As with labor, a .hi-blue[Firm's Demand for Capital]: `$$MRP_K=MP_K* MR(q)$$` - `\(MRP_K\)`: marginal revenue product of capital - `\(MP_K\)`: marginal product of capital - `\(MR(q)\)`: marginal revenue - Firms borrow money today in exchange for promising future repayment with interest - Firms borrow more (less) funds at lower (higher) interest rates ] <img src="capital-slides_files/figure-html/unnamed-chunk-16-1.png" width="504" style="display: block; margin: auto;" /> --- # Demand for Capital .pull-left[ - Note in general, firms are not the only borrowers of funds! - Individuals borrow money to attain higher consumption than their current income - Mortgages, auto loans, student loans, etc. - Governments also borrow money to attain higher spending levels than their current taxation - .blue[Market Demand]+ Demand from Firms + Demand from Individuals + Demand from Government ] <img src="capital-slides_files/figure-html/unnamed-chunk-17-1.png" width="504" style="display: block; margin: auto;" /> --- # Individual Borrowing Decisions .pull-left[ - Again, consider the “life cycle” of decisions - People like to “smooth” their consumption over time, rather than experience sudden, discontinuous jumps in consumption level - When actual income `\(<\)` preferred consumption: **borrow** money - When actual income `\(>\)` preferred consumption: **save** (and lend) money ] .pull-right[ .center[  ] ] --- # Market for Loanable Funds .pull-left[ - Loanable funds market, where .red[savers] and .blue[borrowers] exchange present & future money - Equilibrium market interest rate `\(r^\star\)` ] <img src="capital-slides_files/figure-html/unnamed-chunk-18-1.png" width="504" style="display: block; margin: auto;" /> --- # Market for Loanable Funds .pull-left[ - An increase in .blue[Demand] raises interest rate `\(r\)` and quantity of funds loaned/borrowed ] <img src="capital-slides_files/figure-html/unnamed-chunk-19-1.png" width="504" style="display: block; margin: auto;" /> --- # Market for Loanable Funds .pull-left[ - An increase in .red[Supply] lowers interest rate `\(r\)` and quantity of funds loaned/borrowed ] <img src="capital-slides_files/figure-html/unnamed-chunk-20-1.png" width="504" style="display: block; margin: auto;" /> --- # Capital Markets .pull-left[ .smallest[ - Several mechanisms and types of financial markets by which borrowers and lenders exchange present for future money - .hi[Bond markets]: large companies (and governments) sell an I.O.U. to investors (“bondholders”), and will repay them with interest - .hi[Equity markets]: large companies sells shares of stock to investors (“shareholders”), in exchange for ownership stake - .hi[Banks]: savers deposit funds in bank (and are paid interest), and bank lends the deposits to borrowers (at higher interest rate) ] ] .pull-right[ .center[   ] ]